How Often Should You Sweep Your Mortgage Pipeline for Refi Opportunities?

Manual sweep cadence is the wrong question. Independent mortgage brokers lose refi business to retail lenders not because their sweeps are too slow—but because retail lenders aren't sweeping at all. They're monitoring continuously. The right question is what it takes to replace periodic sweeps with always-on rate monitoring.

Key findings:

- The industry-average refi recapture rate was 37% in Q2 2025, while Rocket Mortgage publicly reports an 83% rate—a 2.2x asymmetry between top servicers and the rest of the market (Mortgage Bankers Association, 2025).

- UWM's Mia—an automated outreach system given free to partner brokers—calls 50 past clients in 3 minutes the moment its rate-drop algorithm fires (National Mortgage Professional, 2026).

- According to industry reporting, roughly 70% of refi recapture opportunities are scooped up by other lenders or servicers before the original broker can act (Floify, via Mortgage News Daily, 2025).

What's the Typical Refi Sweep Cadence for Independent Mortgage Brokers?

There's no standard. Some brokers sweep weekly—rate sheets every Monday, scanning past clients whose math might be in range. Others sweep monthly, quarterly, or only when a borrower calls back asking about rates. Many don't have a true cadence at all; they have an intent ("I should be checking on past clients more") that gets executed when work slows down or when rates drop dramatically.

The reason no cadence has emerged as standard is structural: any cadence longer than daily is too slow, and a daily manual sweep is impossible to sustain at scale. The cadence question itself is the problem—it assumes the work is sweeping, when the actual job is monitoring.

Why Do Manual Sweeps Fail at Any Cadence?

A manual sweep is bounded by attention. You can scan 30 borrower files in an hour. You can't scan 300 in a workday—not while answering calls, drafting loan files, and running your business. Rates move daily; the math depends on today's rates, not last week's.

A diligent broker on a weekly cadence misses 4 business days of fresh signal between sweeps. By Friday morning, a borrower whose math worked Tuesday has already received a "rates dropped" email from a retail lender who watches the market nightly.

According to industry reporting, roughly 70% of refi recapture opportunities are scooped up by other lenders or servicers before the original broker can act (Floify, via Mortgage News Daily, 2025). The 70% gap isn't about who's the better broker. It's about which side started talking to the borrower first.

How Fast Do Retail Lenders Contact Your Borrowers When Rates Move?

UWM's Mia—the wholesale lender's automated outreach system, given free to partner brokers—calls 50 past clients in 3 minutes the moment its rate-drop algorithm fires (National Mortgage Professional, 2026). Larger retail lenders run similar systems: rate movement crosses a threshold; algorithms flag borrowers in seasoning range; calls or emails go out automatically.

The asymmetry is structural. The industry-average refi recapture rate was 37% in Q2 2025, while Rocket Mortgage publicly reports an 83% rate—a 2.2x asymmetry between top servicers and the rest of the market (Mortgage Bankers Association, 2025). Rocket's 83% isn't a function of better brokers. It's a function of always-on monitoring matched with always-on outreach.

What independent brokers have that retail lenders don't is the relationship—the trust and history with the borrower. What they don't have is the tech that turns relationship into recapture before someone else gets there.

What Does Continuous Monitoring Look Like in Practice?

Continuous monitoring isn't a faster sweep. It's a different architecture.

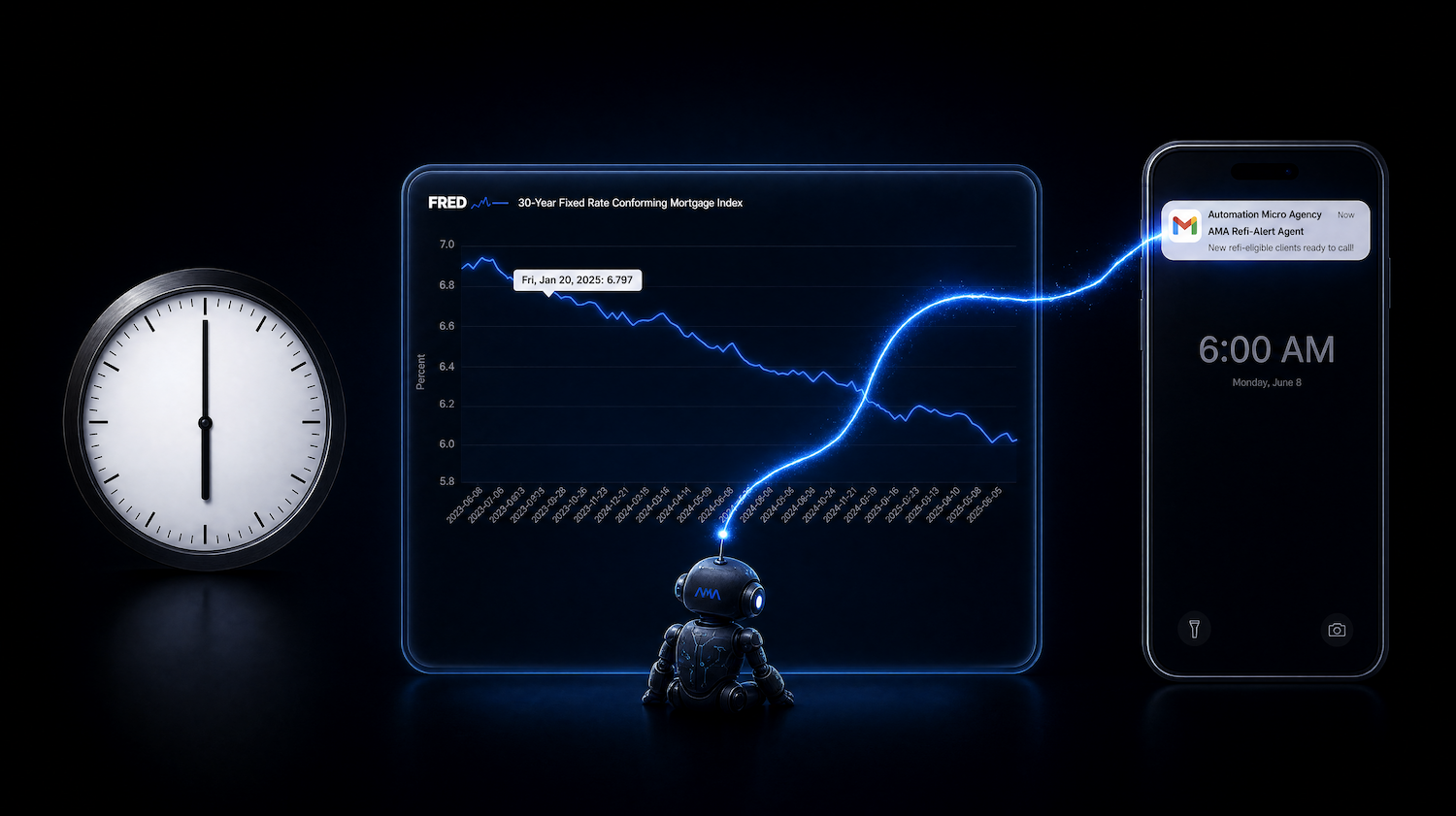

Automated monitoring is continuous in attention. The system polls market rates every business morning; when the day's market rate crosses the threshold that could put borrowers into refi range, it runs break-even math across your closed-loan list.

That architecture trades a small daily polling cost for never missing a day of fresh signal. The output is a short list of names—borrowers whose math now works—delivered the morning rates moved. Your job shifts from sweeping to deciding.

One more design point matters: outreach stays under your control. Automation Micro Agency (AMA)'s Refi-Alert product line defaults to human-in-the-loop: the system identifies opportunities and surfaces them to you; outreach to borrowers stays under your control.

Per-borrower rate checks complete in roughly a second; a 50-borrower sweep finishes in about a minute, not hours. See what this looks like for an independent broker.

Is Automated Monitoring Overkill for a Small Shop?

It depends on what you call small. The same architecture, scaled to a portfolio of 200 or 2,000, runs fine for a small shop. A scoped automated refi-monitoring build typically deploys in 2–4 weeks; it doesn't require enterprise infrastructure or a tech team.

The math test is simpler than the size test: how often do rates move enough to put past borrowers in refi range, and what's a captured refi worth to your book?

In stable rate environments, the system fires infrequently—threshold gating ensures it only flags borrowers when rates have moved enough to matter. In falling-rate environments, triggers cluster as rates cross thresholds for multiple borrowers in quick succession. The system earns its place when the value of a single captured refi exceeds the cost of running the monitoring.

For a fuller breakdown of what AI automation typically costs for a small business, see our post on AI automation cost for small businesses.

The honest answer: monitoring isn't overkill if your past borrowers represent business someone else is competing for. Which, right now, they are.

Frequently Asked Questions

How often should I check rates if I don't automate yet?

The practical floor is weekly—pull rate sheets every Monday, scan past clients whose locked rates are 0.75–1.0% above current market, and flag the ones who'd hit break-even after closing costs. You'll still miss days of signal between sweeps, but a weekly cadence surfaces the most obvious opportunities. Brokers operating less than weekly are better off committing to weekly or moving to automation.

Will I get burned by alert fatigue if the system runs continuously?

No—because the system only fires when rates cross your threshold. You set the threshold; you control the frequency. If alerts feel too frequent, the threshold gets tightened. Continuous monitoring without continuous alerts is the design point.

What if rates aren't moving—does monitoring still pay off?

Rates don't have to move much to create opportunity for borrowers close to the threshold. Even a small drop in 30-year fixed rates can move multiple borrowers in your portfolio into recapture range—if you know which ones to call. In flat-rate environments, the system runs quietly; the moment rates move, you get the names.

If cadence is the wrong question, the right one is what an always-on system actually does on your portfolio. We've laid out exactly that for independent brokers—what gets monitored, how borrower lists get filtered, and where your team stays in the loop on outreach decisions.

See How It Works for Brokers →